|

|

|

ADVERTISEMENTS

|

|

PREMIUM

- HAPPY HOLIDAYS!

- Siliconeer Mobile App - Download Now

- Siliconeer - Multimedia Magazine - email-Subscription

- Avex Funding: Home Loans

- Comcast Xfinity Triple Play Voice - Internet - TV

- AKSHAY PATRA - Bay Area Event - Sat. Dec 6

- Calcoast Mortgage - Home Loans

- New Homes in Silicon Valley: City Ventures - Loden Place - Morgan Hill

- Bombay to Goa Restaurant, Sunnyvale

- Buying, Sellling Real Estate in Fremont, SF Bay Area, CA - Happy Living 4U - Realtor Ashok K. Gupta & Vijay Shah

- Sunnyvale Hindu Temple: December Events

- ARYA Global Cuisine, Cupertino - New Year's Eve Party - Belly Dancing and more

- Bhindi Jewellers - ROLEX

- Dadi Pariwar USA Foundation - Chappan Bhog - Sunnyvale Temple - Nov 16, 2014 - 1 PM

- India Chaat Cuisine, Sunnyvale

- Matrix Insurance Agency: Obamacare - New Healthcare Insurance Policies, Visitors Insurance and more

- New India Bazar: Groceries: Special Sale

- The Chugh Firm - Attorneys and CPAs

- California Temple Schedules

- Christ Church of India - Mela - Bharath to the Bay

- Taste of India - Fremont

- MILAN Indian Cuisine & Milan Sweet Center, Milpitas

- Shiva's Restaurant, Mountain View

- Indian Holiday Options: Vacation in India

- Sakoon Restaurant, Mountain View

- Bombay Garden Restaurants, SF Bay Area

- Law Offices of Mahesh Bajoria - Labor Law

- Sri Venkatesh Bhavan - Pleasanton - South Indian Food

- Alam Accountancy Corporation - Business & Tax Services

- Chaat Paradise, Mountain View & Fremont

- Chaat House, Fremont & Sunnyvale

- Balaji Temple - December Events

- God's Love

- Kids Castle, Newark Fremont: NEW COUPONS

- Pani Puri Company, Santa Clara

- Pandit Parashar (Astrologer)

- Acharya Krishna Kumar Pandey

- Astrologer Mahendra Swamy

- Raj Palace, San Jose: Six Dollars - 10 Samosas

CLASSIFIEDS

MULTIMEDIA VIDEO

|

|

|

|

|

ECONOMY:

The Yin and Yang of U.S. Debt

Growing American debt has consequences for both lenders and borrowers. Chinese institutions hold 10 percent of US Treasuries, but that may not give them the power to move US markets as often assumed, write Ashok Bardhan and Dwight Jaffee.

American homeowners worried about dwindling property values and the burden of adjustable-rate mortgages may not care to know what made their mortgages so affordable. Increased purchase of US Treasury bills, Agency bonds and mortgage-backed securities by foreign government institutions that made mortgages so low, however, has worried economists. With the US economy reeling from multiple shocks, economists have another source for concern – the increasing role played by foreign institutions and sovereign wealth funds, mostly belonging to emerging economies, in financing imports of goods and services to the US that support its lifestyle.

By virtue of the very structure and logic of international trade, the large and continuing purchases of US securities by foreign investors are yin to the yang of the equally large and continuing US trade deficits. Americans buy more than they can pay for. One consequence of purchases by foreigners of US debt securities has been to help lower US interest rates and mortgage rates, with estimates ranging from 50 to 90 basis points. Increasingly, therefore, there exists the corresponding risk of rising interest rates, dollar depreciation or related dislocations were foreign entities to reduce or reverse these purchases. This raises relevant questions: Is this stream of financing sustainable? What could be the consequences of a reversal of these flows?

Although the US current account deficit – the gap between US import of goods and services and its exports – has been checked somewhat by the falling dollar in 2007, it still amounts to over 5 percent of US GDP, and foreign-surplus countries continue to accumulate a greater net amount of dollar-denominated securities. While these facts have been in place for some time, the distinguishing features in recent years have been the cast of investors doing the financing, the extent of their holdings, and their motivations.

As of the middle of 2007, foreign investors held almost $5 trillion in US equities and foreign direct investment, almost $3 trillion of US corporate bonds and more than $2 trillion of US Treasury securities. Foreign ownership of US Agency securities, bonds and mortgage-backed securities (MBS) issued or backed by agencies such as Ginnie Mae, Fannie Mae and Freddie Mac totaled just under $1.5 trillion. While the absolute amounts may be large, it’s the share held by foreign investors of total US securities outstanding that conveys the significance of these global financial flows.

The foreign share of US Treasury securities shows the greatest penetration – almost 45 percent of all US Treasury securities outstanding. This share has grown rapidly, from less than 20 percent of the total as recently as 1994. The foreign share of Agency securities has also grown rapidly, rising from about a 6 percent share in 1994, to over a fifth of the total US Agency securities outstanding. Foreign official institutions, which include central banks, as well as most sovereign wealth funds, own the major share – 74 percent of Treasury securities and 59 percent of Agencies – of these foreign holdings of US debt securities, but only 8 percent of all foreign holdings of US equities.

Asian entities are the most prominent foreign investors, and hold 31 percent of all US Treasuries outstanding, 13 percent of all Agency bonds and Agency-backed mortgage pool securities, but relatively small shares of US corporate bonds and equities, while European investors hold over 16 percent of all US corporate bonds, but relatively small shares of all other security classes. In terms of individual country holdings, Chinese entities hold close to 10 percent of all US Treasuries, 6 percent of Agency bonds and MBS, with much smaller shares of US corporate bonds and equities. Japanese investors claim about 13 percent of US Treasuries, 3.5 percent of US Agency bonds and MBS. Russia and the Middle Eastern oil exporting countries hold smaller shares. Most of the growth in these holdings, particularly those of China, has taken place since 2000.

Recently, there’s been increasing concern regarding the sustainability of these foreign capital inflows, particularly from China, in the wake of the ongoing financial crisis and the depreciating dollar. The impact, in case of a slowdown or a reversal of these flows, will tend to depend on the substitutions and whether the alternative investments stay within the US dollar-denominated universe. For example, a movement by Chinese institutions out of Treasuries and into Agencies, or vice-versa, is unlikely to have much impact on the interest-rate spread, because of their close substitutability, and none on the dollar, both being dollar-denominated.

Diversification into euro-denominated securities, however, would create pressure for the dollar to depreciate relative to the euro. It would also pressure the dollar to depreciate against the Chinese yuan, although how much would depend on the Chinese central bank’s exchange-rate policy at the time. In addition, if the market were to interpret the transaction as a signal of a new Chinese government policy to allow the yuan to float more freely against the dollar, then the exchange-rate adjustment could be swift and large.

Given the focus on China’s intentions and their sizeable holdings, it’s possible that even a minor change in their policy direction vis-à-vis purchases and holdings of US securities could have major impact on the expectations of market participants regarding the future trajectory of the yuan-dollar relationship. At the same time, there would be a sizeable increase in interest rates, both through the price-yield channel and inflationary pressures.

Although there are a number of other significant players, including oil-exporting countries, the future role of China in global capital flows remains critical. Among the reasons given for China’s investments in US securities, the political economy surrounding the maintenance of a relatively undervalued yuan vis-à-vis the dollar to promote exports to the US gets particular prominence. The current development strategy in China seems to rely on an implicit consumption tax created by an undervalued yuan (imported goods cost more), in order to expand export-driven employment and deal with ongoing pressures of job creation.

On the other hand, the case for diversification rests on the low returns on present investments, as well as future fears about the dollar trajectory. The forays into private equity, as well as attempts at other private stakes by the newly government-created China Investment Corporation, tasked to better manage a part of the reserve bonanza have not been particularly successful, and calls increase within China to use the funds for broader social and economic goals in what is after all a developing country, with about 300 million poor, according to recent World Bank estimates.

At the same time, a global shortage of creditworthy debt instruments has created low yields, making it difficult to find productive investments. Also, the major role played by the US institutions in financing global debt and equity operations, regardless of where actual investments are taking place, determines the need for channeling funds through the US. Most foreign investors, and not just China, are therefore on the horns of a dilemma, and the need to ensure good returns on their investment while not wanting to be the last one out of the door gives the situation its knife-edge quality.

Over the past decade or so, the benefits of international trade happen to have paradoxically landed on one of the most land-locked asset classes imaginable, namely US housing and mortgage markets. A global savings glut and emerging economy reserves recycled back into the US managed to create a low-interest environment that indirectly may have fed the current crisis. While foreign investors might be tempted to transfer to non-dollar denominated assets leading to dollar depreciation, inflation and related dislocations, there are slim chances of abrupt change on the part of anyone. Despite recent turmoil, continuing purchases by foreigners indicate that there’s no loss in the appetite for US securities.

|

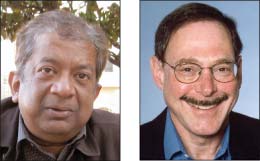

Ashok Bardhan (l) is senior research associate at the Fisher Center for Real Estate & Urban Economics and Dwight Jaffee is professor, Haas School of Business, both at the University of California, Berkeley. Ashok Bardhan (l) is senior research associate at the Fisher Center for Real Estate & Urban Economics and Dwight Jaffee is professor, Haas School of Business, both at the University of California, Berkeley.

This article originally appeared in Yale Global Online (http://yaleglobal.yale.edu/).

© 2008 Yale Center for the Study of Globalization.

|

|

|

|

|

|