REAL ESTATE

To Rent or To Buy?

Owning a Home

Don’t give up on your dream of owning a home because you think you can’t afford it. Realtor Ashok Gupta walks you down the nitty gritty of how to make an informed decision on what could be the most important financial decision in your life.

Given the recent changes in home prices due to short sales and foreclosure and the current low mortgage rate climate, there has been a significant shift in the home affordability for prospective first-time home buyers.

Earlier in 2009, a provision in the Stimulus Bill provided for a first-time Homebuyer Tax Credit of 10 percent of the purchase price of the home up to $8,000, has been extended for a further period on Home purchases by April 30, 2010 and close of escrow by June 30, 2010.

The new bill also allows existing homeowners who had lived in their homes for at least 5 of the last 8 years can buy a second home as a primary residence and get a homebuyer tax credit of up to $6,500.

Young families, having disposable income to buy a home that are still renting were recently interviewed, have a common answer, “We can’t afford one.”

Approaching the task of buying a home can be overwhelming. It is a complex event during which there is so much to learn and to consider. How much can I afford? Where will the down payment come from? How much will I need and where can I find the best loan? How do I begin the look for a home, what should I expect from my real estate agent and what type of home is right for me?

These questions are just the beginning. Buying a home is one of the largest financial transactions in one’s lifetime, yet most people know very little about it. When embarking on the path to home ownership here are two very important points to remember.

First, you can and should understand everything that is happening in the home buying process.

Second, you will need to learn some new terms, apply some new concepts and take the time to learn about purchasing a home.

Always remember that you are the most important person throughout the entire real estate process. It is easy to think that many others may have more expertise or clout, but the truth is that you, the buyer, are the one person in this transaction that makes it all happen. If you decide not to buy, the entire process comes to a complete stop.

If you plan from the beginning to approach the home buying process intelligently and with confidence, you are much more likely to buy the home you’ve always wanted, and have the confidence that the best decisions were made.

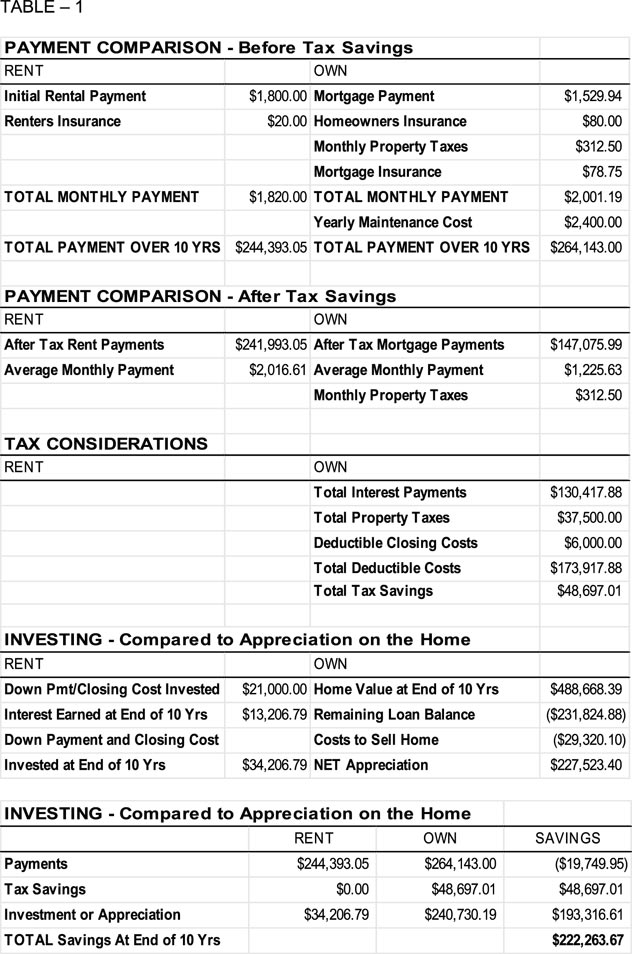

Let us study the logical side of the Renting vs. Buying – A case study based on hypothetical assumptions.

Assumptions:

As a household, you currently rent an apartment at $1,800 per month. You purchase renter’s insurance at a cost of $240 per year or $20 per month. It is assumed that the rent increases 2.5 percent annually over the next 10 years, and that you could earn 5 percent interest on the money that you would have used to pay your down payment and closing costs.

You are now considering the purchase of a home at the entry-level price say $300,000 for a 3 bedroom, 2 bathroom, home which is a little over the statewide median price of $291,800. The monthly cost of housing is equal to the mortgage payment, taxes, and insurance.

The monthly payment including taxes and insurance (PITI) was calculated using a 5 percent or $15,000 down payment, FHA loan at 5 percent fixed for 30 years. Because your down payment is less than 20 percent, we have included mortgage insurance to be paid on a monthly basis. The monthly mortgage payment is $1,529.94 that includes both principal and interest.

NOTE: By buying your home versus renting, you will save $222,263.67 over the next 10 years. The breakdown of this analysis is provided in the table below. Please bear in mind that your decision to buy a home is not only a financial one. There are many emotional reasons for wanting to own the home that you live in, even when the numbers don’t justify the purchase. Please view this analysis as one piece of information to consider as you make this important decision. For the best evaluation of your financial situation, consult your financial advisor. He/she will be the most qualified to discuss the financial consequences of a home purchase decision, as well as help you to establish a plan that will achieve your home ownership goals.

There’s nothing quite like a home that you can truly call your own. A place where you can have the gleaming hardwood floors you’ve always dreamed of, a space to cultivate your own vine-lined patio, a way to provide a good neighborhood for your kids to grow up in, and a freedom from the whims of your landlord. These are the images that immediately come to mind, for many of us.

Yet some of the biggest advantages of owning a home are less romantic and more practical – in fact, there are financial advantages to owning a home.

Tax deductibility. You can deduct the cost of your mortgage loan interest from your state and federal income taxes. Since interest generally will account for most of your payment during the first half of your mortgage, the savings can be significant. Some of your costs at the time of closing (including prepaid mortgage interest) can be taken as deductions on that year’s income tax return, and points paid up front at the time of closing represent additional mortgage interest and may be taken as a deduction.

Tax Deductibility of Property Taxes. You can deduct all of the property taxes you pay.

Appreciation Potential. Real estate is considered a good long-term investment because it usually appreciates in value. The effects of borrowing potential can increase as the value of the home appreciates.

Capital Gains Exclusion. When it’s time to sell your home the amount of capital gains you have to pay is reduced. A homeowner can exclude up to $500,000 per couple if married and filing jointly, or $250,000 if single or filing separately for homes that have been the taxpayer’s principal residence for the previous two years.

Capital Gain Treatment. Congress allows preferential tax treatment on gains from capital assets held for more than one year. This would be important for a homeowner who has gains in excess of the allowable exclusion.

Principal Accumulation. Mortgages are designed to pay the interest for the time that the money has been used, as well as to retire the principal debt over a period of time. This payment plan means that part of the payment each month is for principal accumulation.

Personal Enjoyment. Pride of ownership is a valid reason for wanting to own a home. You can personalize your home while enjoying the financial benefits.

|

Ashok Gupta, CDPE, ePRO is a broker-associate at Intero Real Estate office in Fremont, Calif. He is a

Ashok Gupta, CDPE, ePRO is a broker-associate at Intero Real Estate office in Fremont, Calif. He is a